You're searching for the NC foreclosure timeline because you need to know how long you have. Maybe the letters have already started. Maybe someone mentioned a "notice of hearing" and now you're trying to figure out what that means and how much time is left on the clock.

I get it. When you don't know the timeline, everything feels urgent and vague at the same time. You can't plan your next move if you don't know when the ground shifts beneath you.

So let me lay it out clearly. I'm Ryan Smith, founder of Cinch Home Buyers. I've worked with homeowners across Raleigh, Durham, Charlotte, and a dozen other North Carolina markets — including landowners as far west as Cherokee County — who needed to understand exactly this. The timeline. The deadlines. The moments where you still have choices and the moments where those choices narrow.

If you're behind on your mortgage in North Carolina, here is what's coming, how fast it moves, and what you can do at each stage.

How Long Does the NC Foreclosure Timeline Actually Take?

Here's the short answer: from your first missed payment to a completed foreclosure sale, the NC foreclosure timeline typically runs 90 to 150 days. That's roughly three to five months.

That might sound like a lot of time. But here's what I've learned from talking to hundreds of homeowners in this situation: those months go fast. Especially when you're stressed, unsure of your options, and hoping the problem will resolve on its own.

North Carolina is a non-judicial foreclosure state. That means your lender does not need to file a lawsuit or go through the court system to foreclose. The process runs through a power-of-sale clause that's already built into your mortgage deed of trust. This makes NC foreclosures faster than states that require a judge's involvement.

Let me walk through each phase so you know exactly where you stand.

What Happens at Each Stage of Foreclosure in North Carolina?

Stage 1: Missed payments (Days 1 to 90)

After your first missed payment, your lender will contact you by phone, letter, or both. At this point, nothing formal has happened. You're simply past due.

Most lenders wait until you're 60 to 90 days behind before they escalate. During this window, you have the widest range of options. You can catch up on payments, request a forbearance, apply for a loan modification, or explore selling the property.

This is the stage where most homeowners think they still have plenty of time. And technically, they do. But this is also the stage where waiting costs the most, because the further behind you get, the harder it becomes to catch up. The same window applies to owners trying to sell land in Alexander County before the bank or tax office files — the earlier you move, the more leverage you keep.

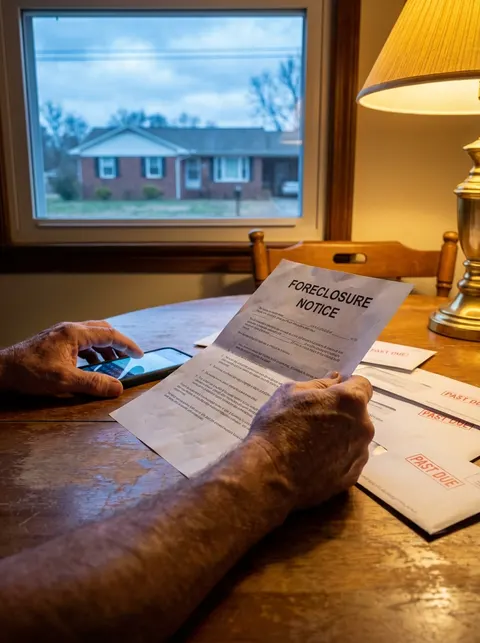

Stage 2: Pre-foreclosure notice (Day 90 to 120)

Once you're about 90 days behind, your lender will send a formal acceleration letter. This letter states that your full loan balance is now due. It's a legal trigger that starts the foreclosure clock.

In North Carolina, the lender must also send a Notice of Hearing at least 10 days before a hearing is held before the Clerk of Superior Court. This hearing determines whether the lender has the right to proceed with foreclosure. The same Clerk-of-Court procedure governs filings in remote counties such as Alleghany County NC — the rules do not relax based on courthouse location.

When you receive a Notice of Hearing, the lender is asking the court's permission to sell your home. You have the right to attend this hearing and present reasons why the sale should not go forward. This is a real window. Many homeowners don't realize they can show up and be heard.

Stage 3: The Clerk's hearing

The Clerk of Superior Court reviews whether the lender has met all legal requirements. If the Clerk authorizes the sale, the foreclosure moves to the next stage. If you can show that you've been making payments, that the lender made errors, or that you have other valid defenses, the Clerk may delay or deny the sale.

After the Clerk's order, you still have 10 days to appeal to a Superior Court judge. This buys you more time, though it doesn't guarantee the foreclosure will stop permanently.

Stage 4: Notice of sale (45-day waiting period)

Once the foreclosure sale is authorized, North Carolina law requires the lender to post a Notice of Sale at least 20 days before the sale date. The notice must also be mailed to you and published in a local newspaper.

There is also a separate 45-day pre-sale notice requirement under NC statute. This means a minimum of 45 days must pass between when you're notified and when the sale can happen.

This 45-day period is what I call your action window. It's the stretch of time where selling the property, catching up on payments, or negotiating with your lender can still stop the sale. For owners of vacant land in Henderson County, that 45-day stretch is often the difference between a clean cash exit and watching a parcel disappear at the courthouse steps. Once the sale happens, the window closes.

Stage 5: The foreclosure sale

The property is sold at public auction, usually at the county courthouse. The highest bidder takes the property. In most cases, the lender bids the amount owed on the loan. If no one outbids them, they take ownership.

After the sale, there is a 10-day upset bid period in North Carolina. During these 10 days, anyone can submit a higher bid (at least 5% more or $750 more than the previous bid). If an upset bid is filed, the process resets for another 10 days. This can extend the timeline, but it also means the sale isn't truly final for at least 10 days after auction.

Stage 6: Eviction

If the property sells and you haven't moved out, the new owner can begin eviction proceedings. In NC, this typically takes an additional 2 to 4 weeks through the courts.

By this point, the foreclosure is on your credit report. Your equity is gone. The timeline for your credit to recover just started its seven-year clock.

"The bank gave me 90 days. Cinch closed in 12. I avoided foreclosure and walked away with equity I thought was gone." — Andre P., Durham

Where on the NC Foreclosure Timeline Can You Still Take Action?

Here's the part that matters most. At almost every stage of this process, you can still do something. The options narrow as time passes, but they don't disappear until the sale is final.

During missed payments (Stage 1): You can reinstate the loan by paying what you owe. You can apply for a modification. You can list the property or sell directly to a cash buyer. Every option is still open.

During pre-foreclosure (Stages 2-3): You can still reinstate in most cases. You can attend the Clerk's hearing. You can negotiate a forbearance. You can sell the property. A cash sale can close faster than a traditional listing, which matters when your timeline is measured in weeks rather than months.

During the 45-day notice period (Stage 4): You can still sell. I've worked with homeowners in Wake County, Durham County, and Mecklenburg County who sold their homes during this window — and our land team has closed Ashe County acreage on the same compressed schedule. We closed in as few as ten days. It was tight. But they walked away with equity instead of a foreclosure on their record.

After the sale (Stage 5+): Your options are limited to the upset bid period. After that, the property belongs to someone else.

The pattern is clear. The earlier you act, the more choices you have. The later you wait, the fewer remain.

| Factor | Let Foreclosure Proceed | Sell Before Foreclosure |

|---|---|---|

| Credit impact | Foreclosure on record for 7 years | No foreclosure on record |

| Equity recovered | $0 (lender takes property) | You keep equity above mortgage balance |

| Future home purchase | 3-7 year waiting period | Can buy again immediately |

| Timeline | 90-150 days (no control) | 10-21 days (your schedule) |

| Privacy | Public auction at courthouse | Private transaction |

| Emotional toll | Eviction by sheriff after sale | You leave on your own terms |

Why Does Understanding the Timeline Change Everything?

When you don't know the timeline, the whole situation feels like a wall coming toward you in the dark. You know it's bad. You know it's getting closer. But you can't see it, so you freeze.

Now you can see it. You know the stages. You know how long each one takes. And that changes the equation, because now you can make decisions based on facts instead of fear.

Selling a home before foreclosure is not giving up. It's using the time you have to protect what's yours. Your equity. Your credit score. Your ability to buy another home in the future.

Homeowners in Raleigh, Durham, Charlotte, and across North Carolina have done exactly this. They looked at the timeline, saw where they stood, and made a move while the window was still open.

At Cinch Home Buyers, we've purchased over 200 properties in 13 NC markets. We've closed in Wake County, Johnston County, Durham County, and Mecklenburg County, and our land arm has bought parcels as far west as Jackson County land in the same pre-foreclosure window. Many of those sales happened during the pre-foreclosure window, and each one gave the homeowner a way to move forward with their finances and their dignity intact.

What Should You Do Right Now?

If you're behind on payments in North Carolina, here's what I'd tell you if you were sitting across from me right now.

First, figure out where you are on the timeline. Look at your most recent letter from the bank. Has the lender sent a Notice of Hearing? Has a sale date been set? Knowing your stage tells you how much time you have.

Second, look at your options honestly. Can you catch up on payments? Can you get a modification? Or has the gap grown too wide? If catching up isn't realistic, selling the property while you still can is the move that protects you most.

Third, talk to someone who knows the process. Not a stranger on the internet. Someone local who has been through this with other homeowners in your area.

That's what we do. Filling out our quick form takes about 60 seconds. We'll review your property and send you a fair cash offer within 24 hours. No obligation. No pressure. No judgment about your situation.

If selling makes sense, we can close on your schedule. If it doesn't, we'll tell you. We're not here to convince you. We're here to make sure you have the information you need to make the right decision for your family.

We buy houses across Wake, Johnston, Durham, and Mecklenburg counties, and we can move on your timeline. You still have a window. Use it.

Frequently Asked Questions

From your first missed payment to a completed foreclosure sale, the NC foreclosure timeline typically runs 90 to 150 days, or roughly three to five months. North Carolina is a non-judicial foreclosure state, meaning your lender does not need to file a lawsuit or go through the court system. The process runs through a power-of-sale clause built into your mortgage deed of trust.

Yes. At almost every stage of the foreclosure process, you can still sell your property. During missed payments, all options are open. During pre-foreclosure, you can sell, attend the Clerk's hearing, or negotiate forbearance. During the 45-day notice period, a cash sale can close in as few as 10 days. After the sale, options are limited to the 10-day upset bid period. The same rule applies if you own raw land instead of a house — sellers in Catawba County, NC use this window the same way.

Once the foreclosure sale is authorized, NC law requires a minimum of 45 days between when you are notified and when the sale can happen. The lender must also post a Notice of Sale at least 20 days before the sale date and publish it in a local newspaper. This 45-day period is your action window where selling the property or negotiating with your lender can still stop the sale.

After a foreclosure sale in North Carolina, there is a 10-day upset bid period during which anyone can submit a higher bid (at least 5% more or $750 more than the previous bid). If an upset bid is filed, the process resets for another 10 days. This means the sale is not truly final for at least 10 days after auction.

Understanding the timeline lets you make decisions based on facts instead of fear. You can identify which stage you are in, how much time you have, and what options remain. Selling a home before foreclosure protects your equity, your credit score, and your ability to buy another home in the future. The earlier you act, the more choices you have.